(Source:Italian Institute for International Political Studies,2026-06-24)

Three years after the launch of a de-risking strategy, Europe has yet to develop a truly common approach towards China. Both last week’s European Council and the previous G7 summit in Paris brought the issue back to the forefront of the political agenda, but without producing a clear consensus. While some member states advocate for a more decisive shift to reduce economic and strategic dependencies on Beijing, others remain more cautious. Their concerns stem not only from the potential economic costs of a rapid deterioration in the relations with China, but also from an increasingly uncertain international environment, shaped also by growing questions regarding the future reliability of transatlantic relations.

Why it matters

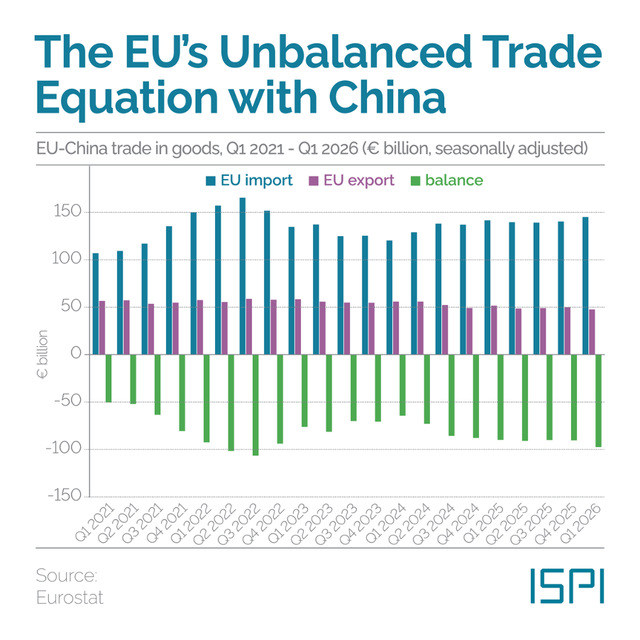

The deficit is here to stay. The EU-China trade imbalance continues to worsen: in 2025, EU exports to China totaled €199.6 billion against €559.4 billion in imports, leading to a deficit of €359.8 billion – exports down 6.5%, imports up 6.4%. In Q1 2026 alone, the deficit reached €98 billion, the highest since Q3 2022. Von der Leyen noted at the G7 that, for the first time, all EU member states recorded a bilateral deficit with China.

Different economies, different approaches. Internal divisions persist, even as the diagnosis converges. While France and Northern European countries increasingly frame the relationship in terms of strategic risk, others remain concerned about the potential costs of a more confrontational approach. In this scenario, Germany remains the most exposed: its exports to China are shrinking while its industrial dependence on Chinese inputs is difficult to unwind. On a different note, Spain has been advocating for a more pragmatic posture, preferring targeted responses to clearly unfair practices over broad instruments that risk retaliation.

New EU’s toolboxes in sight. Beyond existing anti-dumping and anti-subsidy instruments, the Commission has discussed possible plans for an “overcapacity instrument” to restrict Chinese market access in sectors distorted by state-backed overproduction – noting that China accounts for 30% of global industrial output but only 13% of consumption. A parallel proposal would require European firms to source critical components from at least three different suppliers to avoid overreliance on one single source. Beijing has already threatened retaliation if Brussels were to proceed in this direction. Still, the June European Council gave the Commission a mandate to develop a more comprehensive diversification package, but the legal design, sectoral scope and binding force of the new instruments remain undefined.

The big issue: China’s consumption is weak. The structural weakness at the heart of China’s growth model is consumer demand. Household spending remains depressed by a prolonged property crisis which has eroded household wealth and confidence. Moreover, deflationary pressure persists across key sectors, from EVs to e-commerce, as producers trapped by overcapacity resort to aggressive price competition rather than margin recovery. With its 15th Five-Year Plan, the Chinese government has tried to mitigate these effects, setting consumption growth as a priority and targeted subsidies for home appliances and vehicles – but their effect faded quickly. Without structural reforms to household income and the social safety net, domestic demand is unlikely to provide a durable alternative to export-led growth, thus intensifying the pressure on European markets to absorb Chinese overproduction.

Beijing’s trade arsenal. While Brussels debates on which instrument to adopt, Beijing is leveraging its resources. Since April 2025, successive waves of export controls by China on rare earth elements have caused prices in Europe to spike up to sixfold. A broader second wave with extraterritorial reach remains partially suspended until November 2026. However, the licensing architecture keeps expanding: in April 2026, seven EU defense firms – including Germany’s Hensoldt and Belgium’s FN Herstal – have been added to China’s export control list, over alleged arms sales to Taiwan. The ECB estimates over 80% of large European firms are no more than three intermediaries away from a Chinese supplier. Dependency is not a future risk, it is an operational lever already in use.

OUR TAKE

Europe’s window for strategic deliberation is closing fast. While Brussels commissions new instruments and member states negotiate their differences, Beijing continues to act – tightening export controls and licensing administration while deploying trade tools with growing precision against European firms. The underlying fundamentals offer little comfort: China’s structural inability to rebalance toward domestic consumption means its export-driven growth model will continue generating surpluses that widen the EU’s deficit and deepen European dependencies. A shared European awareness of the economic security challenge is no longer enough – it is the baseline. What is now urgently needed is the ability to translate that convergence into enforceable, coordinated action.

Experts’ views

What is the current state of EU-China relations?

The European Council’s 18–19 June 2026 conclusions on competitiveness and global economic challenges are notable for their deliberate vagueness. Leaders conducted a “strategic debate on global macroeconomic imbalances” and urged “decisive progress” on industrial renewal, innovation, reducing dependencies and investment – without once naming China. This lack of specificity indicates that the EU does not want to be perceived as starting a trade war. It is a prudent move. Explicit confrontation or immediate tariffs would risk Chinese retaliation, expose internal divisions and accelerate industrial damage before Europe has credible defensive instruments in place. The open question is whether this approach is only tactical. By keeping the language broad, the Council buys time for the Commission to develop new overcapacity tools over the summer while preserving room for dialogue. The issue returns in October. If these months are used to build unity and concrete leverage, the restraint will prove strategically sound. If it merely defers difficult decisions, Europe will continue ceding ground to China’s structural overcapacity.

Alicia Garcia Herrero, ISPI Senior Advisor

As European leaders convened at the European Council meeting in Brussels this June, the spectre of a full-blown trade war with China cast a long shadow over the proceedings. Yet, beneath the hawkish political rhetoric, recent high-level meetings between European officials and their Chinese counterparts underscore a mutual desire of avoiding a zero-sum confrontation. In fact, the current frictions over provide incentives for the two sides to look beyond short-term political posturing and work on a deal that delivers institutional stability and predictability which is essential for business and mutual trust. One of the key sources of tensions between the EU and China is the diminishing complementarity and increasing competitiveness of the economy. To manage this newly competitive dynamic, the EU and China should engage in a grand bargain rather than a sectoral approach currently adopted by both sides. Negotiating trade disputes sector-by-sector is a game of regulatory whack-a-mole that is insufficient for such a complex relationship. Instead, a grand bargain would establish a comprehensive, overarching framework that is based on China’s enhanced competitiveness as a new economic reality and addresses the EU’s concerns over competitiveness.

Yan Shaohua, Fudan University

WHAT AND WHERE

Xi Jinping’s visit has revived China-North Korea comradeship

In his first foreign visit of the year, Chinese President Xi Jinping headed to Pyongyang to meet the North Korean leader Kim Jong Un. Relations have not been smooth over the past few years, especially after 2020, when North Korea first pursued a strict isolation policy during the pandemic and then privileged strengthening relations with Russia. In fact, the 2-day visit has looked a lot like a charm offensive whereby the Chinese President has sought to regain some of the ground it lost to Vladimir Putin since 2022, when Kim’s pivot towards Russia first became discernible. China is indeed concerned of losing its influence to Russia over a crucial ally for its external security and, during the visit, the language employed by Xi Jinping aimed to underline the Chinese “unwavering support” and “firm commitment to safeguarding the shared interests” of the two countries. These strong-worded proclamations align with Beijing’s recent decisions to resume rail and air link to North Korea, with the likely aim of reviving Chinese tourism there. In the end, the message of the visit is two-faced: on one hand, China does not want North Korea-Russia rapprochement to come at its expense, and on the other Beijing will desist from pushing Kim to relinquish his nuclear arsenal.

Putin courts Southeast Asian leaders

While G7 leaders were meeting to reaffirm their support for Ukraine, Russian President Vladimir Putin was hosting the ASEAN-Russia Summit in Kazan. Marking the 35th anniversary of relations between Moscow and Southeast Asia, the gathering highlighted the growing importance both sides attach to what they describe as a “strategic partnership.” For Russia, closer ties with ASEAN help reduce the impact of Western isolation by opening new markets for energy exports, trade and defence cooperation. For Southeast Asian countries, engagement with Moscow offers an opportunity to diversify external partnerships and avoid excessive dependence on either the United States or China. Several ASEAN members – including the Philippines, Indonesia, Thailand and Vietnam – have imported Russian crude oil or expressed interest in doing so considering the recent Hormuz crisis. More broadly, cooperation with Russia provides additional diplomatic and economic flexibility in an increasingly polarised international environment. The clearest example is Myanmar: since the 2021 military coup, Russia has become one of the junta’s main international backers, providing weapons, diplomatic support and political legitimacy. The relationship reflects mutual interests: Moscow gains influence in a strategically important region, while Southeast Asian countries secure an important partner.

China pressure on Taiwan increases after Takaichi-Marcos summit

Maritime tension is rising in the seas of East Asia. Late last month, when the Philippines’ President Ferdinand Marcos Jr was visiting Japan’s PM Sanae Takaichi, the two leaders issued a joint statement to announce areas of progress where the two countries should deepen their partnership. The prime focus was defence cooperation, but the expressed intention to engage in maritime boundary talks is igniting a new phase of regional confrontation around Taiwan. Japanese and Philippine maritime claims regarding their respective exclusive economic zone (EEZ) overlap in the sea east of Taiwan, a particularly sensitive area when it comes to the security profile of the region. China, which considers Taiwan under its own sovereignty, has criticised the Japan-Philippines proposition declaring their agreement “illegal and void” as it perceives the negotiation to infringe on its territorial (and thus also maritime) claims over the island. For this reason, China has been sending repeated coast guard missions to the area over the last few weeks, including one spearheaded by its largest patrol vessel. The Taiwanese coast guard has opposed Chinese encroachment, dispatching its own vessels to repel the PRC assertions of the maritime jurisdiction. Yet, such lawfare tactics are likely to continue: China has been conducting coast guard operations near Taipei-controlled outlaying islands even before the Japanese-Philippine statement, and the EEZ boundary negotiations offered Beijing the political opportunity to step up its maritime activities around Taiwan.

Myanmar’s leader diplomatic activism while the war continues

Myanmar’s leader Min Aung Hlaing, who led the 2021 military coup and was recently elected as Head of State in a vastly criticised election, has launched an active diplomatic campaign aimed at reducing Myanmar’s isolation and reintegrating the country into the regional political landscape. In recent weeks, he visited India, a key neighbour with which Myanmar shares a long border and a complex relationship shaped by security concerns and migration issues. Despite these challenges, New Delhi sees strategic value in closer ties with Naypyidaw, particularly because it hopes to benefit from Myanmar’s reserves of critical minerals and rare earths. Meanwhile, for Myanmar, stronger relations with India might offer an opportunity to reduce its heavy dependence on China. Min Aung Hlaing’s most significant visit, however, was to Beijing. During a five-day trip last week, the general met Chinese President Xi Jinping, with the two leaders issuing a joint statement reaffirming bilateral cooperation. The meeting underscored China’s continued support for Myanmar’s military-led government, which remains heavily reliant on Beijing for diplomatic backing and economic engagement. Myanmar thus finds itself balancing between Asia’s two giants: India’s growing diplomatic engagement reflects a broader effort to counter China’s influence in its strategic neighbourhood and prevent other countries from becoming too firmly anchored in Beijing’s orbit.

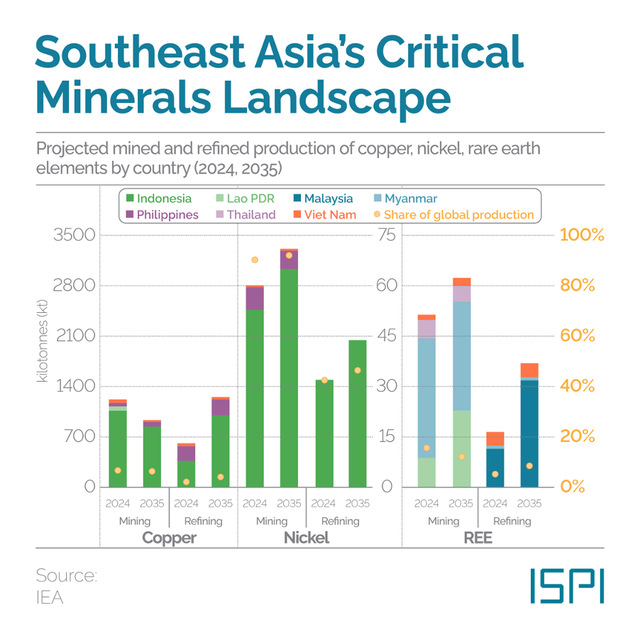

TREND: Critical Minerals in Southeast Asia: Expanding Production, Limited Refining

Southeast Asia is rapidly emerging as a key hub in the global critical minerals landscape. According to IEA projections, the region’s production and processing capacities for copper, nickel and rare earth elements (REEs) are expected to expand markedly by 2035, reflecting growing global demand from clean energy technologies, electric vehicles and advanced manufacturing. Indonesia is set to strengthen its already strong position in the nickel sector, accounting for the vast majority of both mined and refined output. In the REE industry, Myanmar, Malaysia, Laos and Vietnam are projected to play increasingly important roles at different stages of the value chain. Copper production is also expected to grow in the region, although at a more moderate pace and with a more balanced contribution from countries such as Indonesia and the Philippines. At the same time, the data highlights structural tension: while mining output is projected to increase across the region, the development of refining capabilities remains largely uneven. This reflects a long-standing economic model centered on the export of raw materials rather than higher-value industrial activities. For countries seeking to diversify their critical minerals supply chains away from China, Southeast Asia represents both an opportunity and a risk: the region holds the resources, but the refining infrastructure remains largely absent or dependent on Chinese technology and capital.